Buy Now Pay Later: US Consumer Trends 2026

The financial landscape is in constant flux, shaped by technological advancements, shifting consumer behaviors, and evolving economic conditions. Among the most transformative phenomena of the past few years is the meteoric rise of Buy Now, Pay Later (BNPL) services. What began as a niche payment option has rapidly permeated mainstream retail, fundamentally altering how US consumers approach purchasing decisions. As we look towards 2026, understanding the trajectory and implications of BNPL US Trends becomes paramount for consumers, businesses, and regulators alike.

This comprehensive article delves deep into the heart of the BNPL phenomenon in the United States. We will explore the driving forces behind its widespread adoption, dissect the demographic shifts that characterize its user base, and analyze the profound impact it has had on both the retail sector and individual consumer financial health. Furthermore, we will cast our gaze forward to 2026, offering projections on how these services are expected to evolve, the regulatory challenges on the horizon, and the potential future of credit and spending in America.

From the convenience it offers for managing budgets to the potential pitfalls of accumulating debt, BNPL presents a complex picture. By unpacking the nuances of current adoption rates, understanding the psychological underpinnings of its appeal, and anticipating future developments, we aim to provide a holistic view of this powerful financial tool. Join us as we navigate the intricate world of BNPL US Trends and uncover what 2026 holds for this disruptive payment method.

The Genesis and Growth of Buy Now, Pay Later in the US

The concept of installment payments is far from new, but the digital transformation and consumer-centric approach of modern BNPL services have revolutionized its application. Historically, layaway plans allowed consumers to pay for goods over time, receiving the item only after full payment. Credit cards, on the other hand, offered immediate gratification with revolving credit. BNPL services, such as Affirm, Afterpay, Klarna, and Sezzle, bridge this gap by offering immediate possession of goods or services coupled with a structured, often interest-free, installment payment plan. This hybrid model has struck a chord with a significant segment of the US population, particularly those seeking alternatives to traditional credit or looking for more flexible budgeting tools.

The initial surge in BNPL adoption can be traced back to several key factors. The COVID-19 pandemic, with its acceleration of e-commerce and economic uncertainties, played a pivotal role. As consumers shifted more of their spending online and sought ways to manage their finances amidst fluctuating incomes, BNPL offered a convenient and seemingly low-risk solution. The perception of BNPL as a ‘smarter’ or ‘safer’ alternative to credit cards, often due to the absence of interest charges for on-time payments, further fueled its growth. Furthermore, the seamless integration of BNPL options at online checkout points made it an effortless choice for impulse purchases and larger ticket items alike.

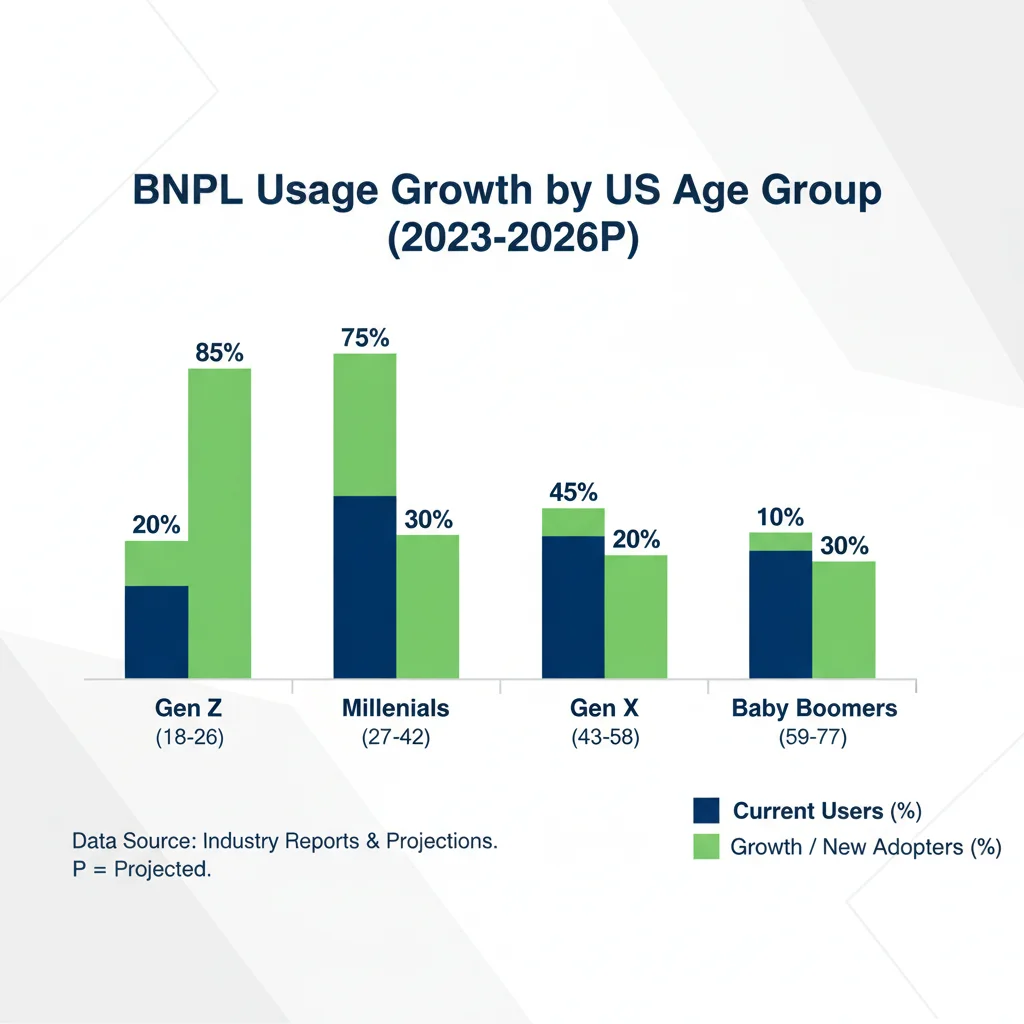

Early adopters were predominantly younger demographics, particularly Gen Z and Millennials, who were either credit-averse, had limited credit history, or preferred transparent payment schedules over the complexities of traditional credit card statements. However, the appeal of BNPL has since broadened, attracting a more diverse user base across all age groups and income brackets, underscoring its widespread utility and adaptability. This expansion signifies a fundamental shift in consumer payment preferences and habits, making BNPL US Trends a critical area of study for anyone involved in finance or retail.

Key US Consumer Adoption Trends Towards 2026

As we hurtle towards 2026, several distinct trends in US consumer adoption of BNPL are becoming increasingly clear. These trends are not merely statistical anomalies but reflect deeper changes in financial literacy, digital comfort, and economic realities. Understanding these patterns is crucial for businesses aiming to cater to evolving consumer demands and for individuals making informed financial choices.

Demographic Shifts and Broadening Appeal

While initially popular among younger, digitally native generations, the demographic reach of BNPL is expanding rapidly. Surveys indicate a significant increase in adoption among Gen X and even Baby Boomers, particularly for larger purchases like home appliances, electronics, and travel. This broadening appeal suggests that the convenience and budgeting benefits of BNPL are universally attractive, transcending generational divides. By 2026, we can expect BNPL to be a standard payment option for a majority of online and even in-store transactions for a wide cross-section of the US population.

The rise of BNPL is also tied to shifts in income levels and financial stability. For those with stable incomes but who prefer not to use credit cards or deplete savings for immediate purchases, BNPL offers a valuable budgeting tool. For others facing tighter budgets, it provides a means to acquire necessary goods or services that might otherwise be out of reach, spreading the cost over manageable installments. This dual utility underscores its versatility and explains its broad market penetration as a key aspect of BNPL US Trends.

Integration Across Retail Sectors

BNPL is no longer confined to fashion or electronics. Its integration is rapidly expanding across diverse retail sectors, including healthcare (for elective procedures or dental work), travel (for flights and accommodations), and even automotive (for repairs or accessories). This widespread integration makes BNPL a ubiquitous payment option, further embedding it into the daily financial lives of consumers. Retailers who do not offer BNPL risk losing customers to competitors who do, making it an essential component of a modern payment strategy.

The ease of integration for merchants, often through simple API connections, has also accelerated this trend. Many e-commerce platforms now offer BNPL as a native checkout option, reducing friction for both consumers and businesses. This seamless experience is a major driver of continued adoption and a significant factor in shaping future BNPL US Trends.

The Impact of Mobile-First Strategies

The vast majority of BNPL transactions occur via mobile devices. The convenience of applying for and managing installment plans through user-friendly apps is a significant draw. Providers are continually enhancing their mobile interfaces, offering personalized spending insights, payment reminders, and seamless integration with digital wallets. This mobile-first approach aligns perfectly with contemporary consumer habits, where smartphones are central to nearly every aspect of daily life, including financial management. The continued innovation in mobile app functionality will be a critical determinant of how BNPL US Trends evolve.

Blurring Lines with Traditional Credit

As BNPL matures, the lines between it and traditional credit products are beginning to blur. Some BNPL providers are now offering longer payment terms, larger loan amounts, and even interest-bearing options for specific purchases. This evolution could see BNPL services becoming more akin to short-term personal loans, albeit with a focus on point-of-sale integration. This convergence presents both opportunities for greater financial inclusion and challenges regarding regulatory oversight, which we will discuss further.

The Economic and Retail Ramifications of BNPL

The proliferation of BNPL services has had a profound ripple effect across the US economy, impacting retail sales, consumer debt levels, and the competitive landscape for financial services. Understanding these broader implications is essential for a comprehensive grasp of BNPL US Trends.

Boost to Retail Sales and Average Order Value (AOV)

For retailers, BNPL has proven to be a powerful tool for increasing sales and average order value (AOV). By breaking down large purchases into smaller, more manageable installments, BNPL reduces the psychological barrier to spending. Consumers are more likely to complete a purchase, add more items to their cart, or opt for higher-priced goods when they have the flexibility of deferred payments. This has been a significant boon for e-commerce, where cart abandonment rates can be high. Retailers frequently report double-digit increases in conversion rates and AOV after implementing BNPL options.

The competitive advantage offered by BNPL is also forcing more merchants to adopt these services. As more consumers come to expect BNPL at checkout, retailers who don’t offer it risk being perceived as outdated or less customer-friendly. This creates a positive feedback loop, further accelerating the adoption of BNPL across the retail ecosystem, solidifying its place in future BNPL US Trends.

Impact on Consumer Debt and Financial Health

While BNPL offers budgeting flexibility, it also carries potential risks for consumer financial health. The ease of access and the perception of being ‘interest-free’ can lead some consumers to overextend themselves, accumulating multiple BNPL loans across different providers. If payments are missed, late fees can quickly accrue, and in some cases, interest may be applied. Furthermore, while many BNPL providers do not report to traditional credit bureaus for every transaction, missed payments can sometimes negatively impact credit scores, or collections activity can certainly affect them.

The lack of a centralized reporting system for BNPL loans means that consumers can potentially take on more debt than they can comfortably manage, as each provider may not have a full picture of the consumer’s total BNPL obligations. This fragmented view of consumer debt is a growing concern for financial wellness advocates and regulators, and it’s an area that will undoubtedly see changes as part of the broader BNPL US Trends discussion moving into 2026.

Competition with Traditional Credit Products

BNPL has emerged as a significant competitor to traditional credit cards, especially for smaller, short-term purchases. For consumers who are wary of high-interest rates or annual fees associated with credit cards, BNPL offers an attractive alternative. This competition is pushing credit card companies to innovate, with some introducing their own installment payment options or partnering with existing BNPL providers. The long-term impact on the credit card industry remains to be fully seen, but it’s clear that BNPL has carved out a substantial market share, influencing the strategies of established financial institutions.

Beyond credit cards, BNPL also competes with personal loans and even payday loans, offering a more reputable and often more affordable option for short-term financing. This competitive pressure is a key factor shaping the evolving landscape of consumer finance and the future of BNPL US Trends.

Regulatory Landscape and Consumer Protection in 2026

The rapid expansion of BNPL has naturally drawn the attention of regulators concerned about consumer protection, market fairness, and systemic risk. As we approach 2026, the regulatory framework surrounding BNPL in the US is expected to become more formalized and comprehensive. This will be a critical development influencing all future BNPL US Trends.

Federal and State-Level Scrutiny

Currently, BNPL services often operate in a grey area, falling outside some of the stringent regulations that govern traditional credit products under acts like the Truth in Lending Act (TILA). However, agencies like the Consumer Financial Protection Bureau (CFPB) have expressed increasing concerns about the potential for consumers to accrue unsustainable debt, the lack of robust dispute resolution mechanisms, and the transparency of terms and conditions. The CFPB has already initiated inquiries into major BNPL providers, signaling a clear intent to impose greater oversight.

At the state level, some jurisdictions are also exploring legislation to specifically regulate BNPL products, addressing issues such as licensing requirements, interest rate caps, and enhanced disclosure mandates. By 2026, it is highly probable that a patchwork of federal and state regulations will be in place, aiming to strike a balance between fostering innovation and safeguarding consumer interests.

Focus on Transparency and Disclosure

A key area of regulatory focus will be on enhancing transparency. Consumers often perceive BNPL as ‘free credit,’ but late fees and the potential for credit score impacts are significant considerations. Regulators will likely push for clearer, more prominent disclosures of all fees, payment schedules, and the consequences of missed payments. This will empower consumers to make more informed decisions and mitigate the risk of unexpected financial burdens, directly influencing how BNPL US Trends are perceived and utilized.

Credit Reporting and Underwriting Standards

The fragmented nature of BNPL credit reporting is another area ripe for reform. As BNPL services become more integrated into the financial system, there will be increasing pressure for providers to report payment activity to major credit bureaus, both positive and negative. This would provide a more complete picture of a consumer’s financial obligations, aiding in responsible lending decisions across all credit products. Standardized underwriting practices for BNPL loans, potentially incorporating more robust affordability checks, are also likely to emerge, further shaping the operational aspects of BNPL US Trends.

Dispute Resolution and Consumer Rights

Currently, consumer protections for BNPL transactions can vary significantly compared to credit card purchases. Regulators are likely to address this disparity, ensuring that consumers have clear avenues for disputing charges, returning faulty goods, and resolving other issues without being liable for payments on unsatisfactory purchases. This aligns BNPL more closely with the consumer protections afforded by traditional credit cards, promoting greater trust and reliability in the service.

The Future of BNPL: Projections for 2026 and Beyond

Looking ahead to 2026, the landscape of BNPL in the US is poised for continued evolution and significant transformation. The interplay of technological innovation, regulatory adjustments, and shifting consumer expectations will dictate its trajectory. Here are some key projections for future BNPL US Trends.

Consolidation and Diversification of Providers

The BNPL market has seen a proliferation of new players. As the industry matures and faces increased regulatory scrutiny, we can expect a period of consolidation. Larger, more established fintech companies and traditional financial institutions are likely to acquire smaller BNPL startups, leading to fewer, but more robust, providers. Additionally, existing providers will diversify their offerings, moving beyond simple installment plans to include loyalty programs, budgeting tools, and potentially even banking services, creating a more integrated financial ecosystem.

Increased Personalization and AI Integration

Artificial intelligence and machine learning will play an increasingly significant role in BNPL. AI will enable more sophisticated credit assessments, personalized payment plans tailored to individual financial situations, and proactive alerts to help consumers manage their spending. This level of personalization will enhance the user experience and potentially reduce default rates, making BNPL an even more attractive option for a wider range of consumers. This technological advancement will be a cornerstone of future BNPL US Trends.

Expansion into B2B and Services Sectors

While primarily consumer-focused, BNPL concepts are beginning to trickle into business-to-business (B2B) transactions and the services sector. Small businesses could utilize BNPL-like structures to manage cash flow for inventory purchases or equipment upgrades. Similarly, services like home repairs, educational courses, or even medical treatments could see broader adoption of installment payment options, extending the reach of BNPL beyond traditional retail goods.

The Evolving Role of Financial Education

As BNPL becomes more pervasive, the need for robust financial education will become even more critical. Consumers will need to understand the nuances of these services, including how they differ from credit cards, the implications of missed payments, and strategies for responsible usage. Financial institutions, regulators, and BNPL providers themselves will likely collaborate on initiatives to improve financial literacy, ensuring that consumers can harness the benefits of BNPL while mitigating its risks. This educational push will be vital for healthy BNPL US Trends.

Challenges and Opportunities for BNPL in 2026

Despite its rapid growth, the BNPL market faces several challenges and presents numerous opportunities as we look towards 2026. Navigating these will be key to its sustained success and integration into the broader financial system.

Challenges:

- Regulatory Uncertainty: The evolving regulatory landscape, while necessary for consumer protection, could introduce compliance burdens and operational complexities for BNPL providers, potentially slowing innovation or increasing costs.

- Risk of Over-Indebtedness: The ease of accumulating multiple BNPL loans remains a significant concern. A downturn in the economy could expose vulnerabilities in consumers’ financial health, leading to higher default rates.

- Competition: The market is becoming increasingly crowded, not only with other BNPL providers but also with traditional banks and credit card companies offering similar installment options. This intense competition could squeeze profit margins and force consolidation.

- Credit Reporting Integration: The lack of comprehensive credit reporting for all BNPL transactions can make it difficult for lenders to assess a borrower’s overall financial picture, potentially leading to increased risk for both consumers and providers.

Opportunities:

- Financial Inclusion: BNPL can serve as an entry point for individuals with thin or no credit files to build a positive payment history, potentially leading to access to broader financial products.

- Innovation in Payment Solutions: The competitive nature of the BNPL market drives continuous innovation in user experience, payment flexibility, and integrated financial tools.

- Partnerships and Ecosystem Building: Collaborations between BNPL providers, traditional banks, and retailers can create seamless and comprehensive financial ecosystems, offering consumers a wider array of options.

- Global Expansion: While this article focuses on US trends, the success of BNPL in the US could serve as a model for expansion into other global markets, driving further growth for leading providers.

Conclusion: Navigating the BNPL Future

The Buy Now, Pay Later phenomenon has irrevocably altered the US consumer finance landscape. Its rise has been swift and disruptive, driven by consumer demand for flexibility, transparency, and a modern alternative to traditional credit. As we look towards 2026, it’s clear that BNPL is not a fleeting trend but a fundamental shift in payment preferences, deeply embedded in the fabric of digital commerce and increasingly, in-store transactions.

The future of BNPL US Trends will be characterized by continued innovation, a more mature regulatory environment, and a greater emphasis on responsible lending and consumer education. While challenges related to potential over-indebtedness and regulatory harmonization remain, the opportunities for financial inclusion, enhanced consumer choice, and retail growth are substantial.

For consumers, understanding the terms and conditions, managing multiple BNPL accounts diligently, and being aware of the impact on credit scores will be paramount. For businesses, integrating BNPL as a core payment option and adapting to evolving consumer expectations will be crucial for staying competitive. And for regulators, striking the right balance between fostering innovation and safeguarding consumer financial well-being will define the success of BNPL in the years to come. The journey of BNPL is far from over; 2026 will undoubtedly mark another significant chapter in its fascinating evolution.