Gig Economy’s Impact on US Consumer Spending: 3 Key Trends for 2026

The American economic landscape is in constant flux, a dynamic tapestry woven with threads of innovation, technological advancement, and evolving work paradigms. Among the most significant forces reshaping this landscape is the burgeoning gig economy. No longer a niche phenomenon, contract, freelance, and on-demand work has permeated nearly every sector, fundamentally altering how Americans earn, spend, and perceive financial stability. Understanding the gig economy’s influence on US consumer spending patterns is not merely an academic exercise; it’s a critical imperative for businesses, policymakers, and individuals aiming to thrive in the coming years.

As we cast our gaze towards 2026, the implications of this shift become even more pronounced. The flexibility, autonomy, and often supplemental income offered by gig work are driving new consumption behaviors, creating both opportunities and challenges. From the rise of micro-transactions to a redefinition of luxury and essential spending, the ripple effects are far-reaching. This comprehensive exploration will delve into three pivotal trends that are poised to redefine US consumer spending patterns by 2026, all stemming from the pervasive growth and maturation of the gig economy. By dissecting these trends, we can better anticipate the future of commerce, investment, and personal finance in an increasingly gig-centric world.

The Rise of Discretionary ‘Micro-Spending’ Driven by Flexible Income

One of the most immediate and observable impacts of the gig economy on US consumer spending is the proliferation of ‘micro-spending’ – frequent, smaller discretionary purchases often funded by the flexible and immediate income streams characteristic of gig work. Unlike traditional salaried employment, where income arrives in larger, less frequent installments, gig workers often receive payments daily, weekly, or upon completion of specific tasks. This immediate access to funds, even in smaller amounts, fosters a psychological shift in spending habits.

Consider a gig worker who completes several deliveries in an afternoon. The earnings from these tasks are often available almost instantly. This instant gratification of income can lead to instant gratification in spending. Instead of saving up for a larger purchase, consumers might be more inclined to treat themselves to a premium coffee, an on-demand meal, a subscription service, or a small entertainment purchase. These individual transactions, while seemingly insignificant, accumulate to form a substantial portion of overall consumer spending.

By 2026, this trend is expected to intensify. As more individuals engage in gig work, either as a primary source of income or to supplement their earnings, the volume of these micro-transactions will soar. Businesses that successfully tap into this new spending pattern will be those offering immediate value, convenience, and services that align with the on-demand nature of gig work. Think about the growth of quick commerce, streaming services, and app-based purchases – these are perfectly positioned to capture the ‘micro-spending’ dollar. The psychological barrier to making a small purchase when funds are readily available is lower, leading to increased overall consumption in these categories.

Furthermore, the increased financial agility offered by gig work allows consumers to respond more rapidly to economic fluctuations. A sudden need for cash can be met by taking on additional gigs, which then translates into immediate spending power. This contrasts sharply with traditional employment, where an unexpected expense might require dipping into savings or waiting for the next paycheck. This responsiveness creates a more fluid and less predictable spending environment, yet one that is robust in its ability to quickly inject funds into the economy through these smaller, frequent purchases. The gig economy spending trends are clearly pointing towards a future dominated by instant transactions.

This trend also has implications for personal finance. While the flexibility is appealing, managing numerous small income streams and matching them with micro-spending requires a new approach to budgeting and financial planning. Financial technology (FinTech) solutions that help gig workers track income, manage expenses, and even automate savings from these smaller, more frequent deposits will become increasingly vital. The shift isn’t just about how money is spent, but how it’s managed, reflecting a deeper transformation in financial behavior driven by the gig economy.

Shifting Priorities: From Long-Term Investments to Short-Term Experiences and Flexibility

The inherent instability and lack of traditional benefits often associated with gig work are prompting a significant re-evaluation of financial priorities among US consumers. For many gig workers, the traditional path of long-term investments – such as homeownership, extensive retirement planning, or significant capital purchases – becomes less accessible or less appealing. Instead, there’s a growing emphasis on short-term financial resilience, liquidity, and spending that enhances immediate quality of life and provides flexibility.

By 2026, we anticipate a more pronounced shift in how consumers allocate their disposable income. Instead of pouring every extra dollar into a down payment for a house, gig workers might prioritize spending on experiences – travel, dining out, entertainment, or personal development courses that can enhance their skill set and future earning potential in the gig market. This isn’t to say long-term planning is entirely abandoned, but rather that the balance is shifting. The psychological need for immediate gratification and the desire to enjoy the present, given the uncertain nature of future income, become more dominant factors in spending decisions. This is a core aspect of gig economy spending trends.

The ‘asset-light’ lifestyle also gains traction. Owning a car, for instance, might be replaced by relying on ride-sharing services or car-sharing platforms, especially for those in urban areas who don’t need a vehicle for their gig work. Similarly, subscription models for everything from clothing to software become more attractive than outright ownership, offering flexibility and reducing upfront costs. This preference for access over ownership is a direct reflection of the gig economy’s influence, where flexibility and adaptability are paramount.

This trend has profound implications for industries traditionally reliant on large, infrequent purchases. Real estate, automotive, and certain luxury goods sectors may need to adapt their strategies to cater to a consumer base that values flexibility and experiences over long-term, fixed assets. On the other hand, sectors offering adaptable services, short-term rentals, experiential travel, and skill-building platforms are likely to see significant growth.

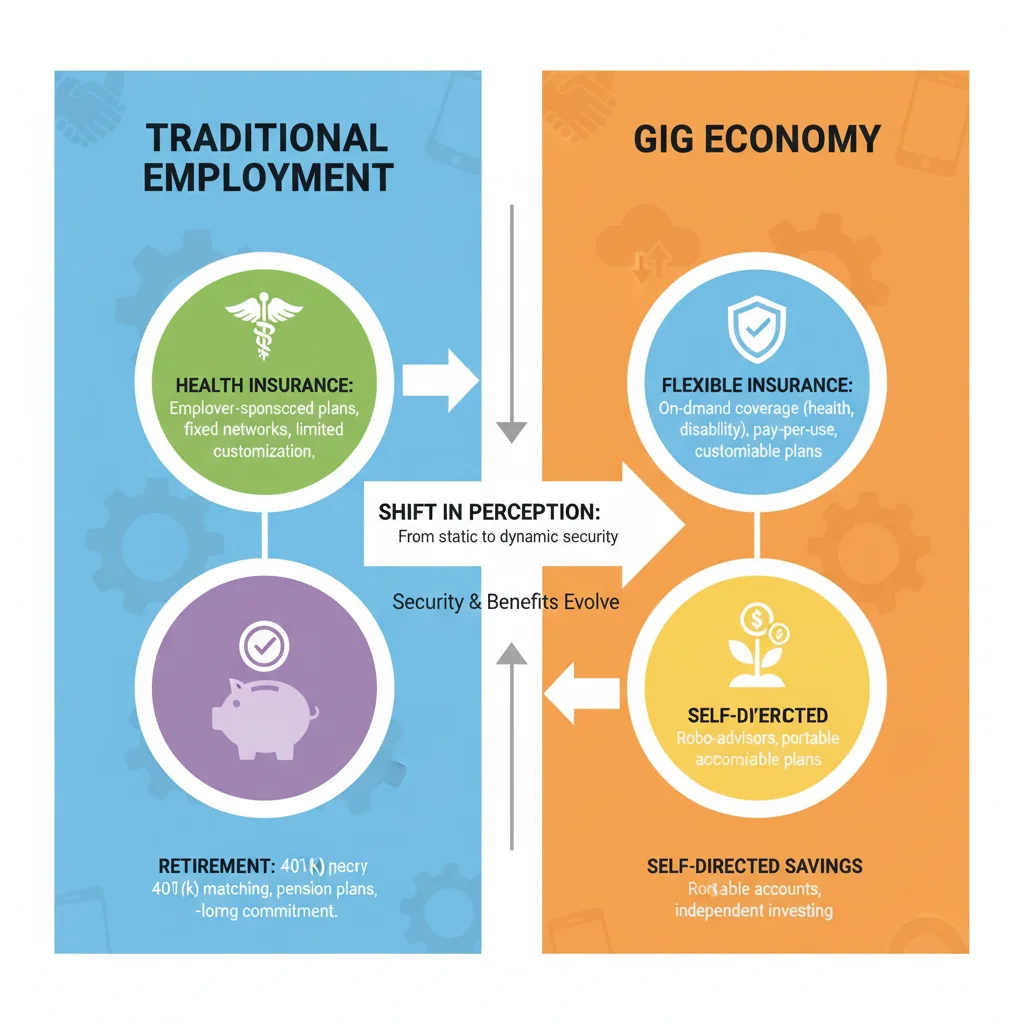

Furthermore, the absence of employer-provided benefits like health insurance and retirement plans compels gig workers to allocate a portion of their income towards these necessities, albeit often through different, more flexible channels. This means a greater portion of their earnings might go towards purchasing individual health insurance plans or contributing to self-directed retirement accounts, impacting the amount available for other types of discretionary spending. This isn’t necessarily a negative trend; rather, it’s a re-prioritization that businesses must acknowledge when targeting this demographic. The focus shifts to immediate needs and adaptable solutions, cementing the gig economy spending trends.

The emphasis on flexibility also extends to how consumers view their living situations. Renting, especially in areas with robust gig opportunities, may become more appealing than buying, as it offers the freedom to move and adapt to changing work demands without the burden of property ownership. This further reinforces the ‘asset-light’ mindset and the prioritization of short-term adaptability over long-term, fixed commitments. The gig economy is not just changing how people work; it’s changing how they live and what they value financially.

The Democratization of Luxury and the ‘Premiumization’ of Essentials

The gig economy, by providing diverse income streams and greater control over work schedules, is subtly but significantly democratizing access to what were once considered luxury goods and services. At the same time, it is driving a ‘premiumization’ of everyday essentials, as consumers seek value, convenience, and improved quality in their routine purchases. These two facets, while seemingly contradictory, are deeply interconnected and will shape US consumer spending by 2026.

On the one hand, the ability to earn supplemental income through gig work means that a broader segment of the population can now afford occasional indulgences that were previously out of reach. A barista working a full-time job might pick up a few evening rideshare shifts to fund a weekend getaway, a designer might take on a freelance project to buy a high-end gadget, or a student might deliver food to afford a concert ticket. These are not grand, life-altering purchases, but rather accessible luxuries that enhance daily life and provide a sense of reward for hard work and flexibility. This democratization means brands in the accessible luxury segment – from fashion to travel to technology – have an expanding market.

Conversely, the premiumization of essentials is driven by the gig worker’s need for efficiency, reliability, and quality in tools and services that support their work and lifestyle. A gig worker might be willing to pay more for a reliable, fast internet connection, a comfortable and ergonomic workspace setup (even if it’s at home), high-quality headphones for calls, or premium meal delivery services that save time. These aren’t luxuries in the traditional sense, but rather essential investments that enable them to perform their work effectively and maintain a reasonable quality of life amidst demanding schedules. The gig economy spending trends highlight this dual shift.

By 2026, businesses that understand this dual dynamic will be best positioned for success. Companies that offer ‘luxe-for-less’ experiences, subscription boxes for curated goods, or premium versions of everyday services will find a receptive audience. The focus is on value proposition – not necessarily the lowest price, but the best combination of quality, convenience, and perceived benefit that justifies the cost. This trend is also fueled by social media, where sharing experiences and showcasing personal style is prevalent, further encouraging aspirational spending on accessible luxuries.

The challenge for businesses will be to differentiate between genuine premiumization (where quality and utility justify higher prices) and simple price inflation. Consumers, particularly gig workers who are often acutely aware of the value of their time and effort, will be discerning. They will seek out brands that genuinely enhance their lives, whether through a delightful, affordable luxury or an essential service that makes their work or daily routine smoother. The gig economy is fostering a generation of savvy consumers who are willing to pay for what truly adds value, redefining the boundaries between necessity and indulgence.

This shift also implies a greater demand for ethical and sustainable consumption. As consumers gain more autonomy over their work, many also seek to align their spending with their values. Brands that demonstrate social responsibility, environmental consciousness, and fair labor practices may find favor even at a slightly higher price point, as gig workers increasingly prioritize meaning and impact alongside functionality and price. This represents a mature evolution of consumer behavior influenced by the flexibility and personal agency found in the gig economy.

Implications for Businesses and Policy Makers

The seismic shifts in US consumer spending driven by the gig economy carry profound implications for a wide array of stakeholders. For businesses, understanding these gig economy spending trends is no longer optional; it’s existential. Companies must re-evaluate their product offerings, marketing strategies, and distribution channels to align with the new realities of micro-spending, a preference for flexibility over long-term assets, and the democratization of luxury alongside the premiumization of essentials.

Businesses in the retail sector, for instance, should consider optimizing for smaller, more frequent purchases, perhaps through subscription models or loyalty programs that reward consistent, small-scale engagement. E-commerce platforms that offer rapid delivery and flexible payment options will continue to thrive. The food and beverage industry will see continued growth in delivery services and convenient, high-quality ready-to-eat options. Brands selling aspirational goods should focus on making them accessible and framing them as rewards for personal effort, rather than as symbols of traditional status.

Service industries, particularly those related to personal wellness, skill development, and experiential travel, are well-positioned for growth. Gig workers, often operating with less structured schedules, have a greater need and opportunity for self-care, continuous learning, and leisure, provided these are offered with flexibility and value. Financial institutions, too, face a critical need to innovate. Developing banking products, investment vehicles, and insurance solutions tailored to the irregular income and varied needs of gig workers will be crucial. This includes simplified tax tools, automated savings from micro-deposits, and flexible insurance options.

For policymakers, the gig economy’s influence on consumer spending highlights the urgent need for updated social safety nets and regulatory frameworks. The traditional employer-employee model, which underpins much of current labor law and benefits provision, is increasingly outmoded. Policymakers must explore portable benefits models that allow gig workers to accrue health insurance, retirement savings, and other protections independently of a single employer. Such measures would not only provide much-needed security for gig workers but also potentially free up more discretionary income, further stimulating consumer spending across various sectors.

Furthermore, understanding the spending patterns of gig workers can inform economic development strategies. Cities and regions looking to attract and retain gig talent might invest in infrastructure that supports their lifestyle – affordable co-working spaces, reliable public transport, and access to high-speed internet. Policies that foster financial literacy and provide guidance on managing irregular income streams will also empower gig workers to make more informed spending and saving decisions, contributing to overall economic stability. The gig economy is not just changing how people consume; it’s changing the very fabric of local economies.

The Future of US Consumer Spending: Adapting to the Gig Economy

The gig economy is not a fleeting trend; it is a fundamental restructuring of work that will continue to evolve and deepen its impact on US consumer spending patterns well beyond 2026. The three trends explored – the rise of discretionary micro-spending, the shift towards short-term experiences and flexibility over long-term fixed assets, and the democratization of luxury coupled with the premiumization of essentials – are interconnected facets of a larger transformation. This transformation is driven by a workforce that values autonomy, flexibility, and immediate gratification, while also navigating the inherent uncertainties of non-traditional employment.

For individuals, adapting to these gig economy spending trends means embracing new approaches to financial planning. Budgeting tools that can handle irregular income, diversifying income streams, and prioritizing financial resilience will become standard practices. It also means being more discerning consumers, seeking value and utility in every purchase, whether it’s a small indulgence or an essential service. The gig worker of 2026 will be a financially agile and experience-driven consumer, constantly weighing immediate gratification against future stability.

For businesses, the imperative is clear: innovate or be left behind. This involves not just adjusting product lines but re-thinking the entire customer journey. Personalization, convenience, and a deep understanding of the gig worker’s unique needs and aspirations will be key differentiators. Companies that can offer flexible payment options, on-demand services, and products that enhance both work and leisure will capture a significant share of this evolving market. Furthermore, businesses have an opportunity to support the gig economy ecosystem by providing services that address its challenges, such as specialized insurance, financial planning tools, and professional development platforms.

Ultimately, the gig economy’s influence on US consumer spending is creating a more dynamic, responsive, and perhaps more equitable marketplace. While challenges related to worker benefits and financial stability remain, the sheer adaptability and entrepreneurial spirit of the gig workforce are driving innovation in consumption. By understanding and proactively responding to these trends, all stakeholders can contribute to a more robust and resilient economic future, ensuring that the benefits of the gig economy are widely shared and its challenges effectively mitigated. The future of US consumer spending is undoubtedly gig-infused, and those who prepare now will be the ones to lead in 2026 and beyond.