Unlock 2% Back on Everything: Your 2026 Credit Card Rewards Blueprint

In an increasingly complex financial landscape, optimizing your spending is no longer a luxury but a necessity. For the savvy consumer, the goal isn’t just to spend wisely, but to ensure every dollar spent works for them. This brings us to the holy grail of credit card rewards: consistently earning 2% back rewards on all your spending. While many cards offer elevated rewards in specific categories, achieving a flat 2% or more across the board requires a well-thought-out strategy, especially as we look towards 2026 and beyond. This comprehensive guide will walk you through the blueprint for making every purchase count, transforming your everyday spending into significant savings and rewards.

The allure of 2% back rewards is undeniable. Imagine getting back $20 for every $1,000 you spend, effortlessly. Over the course of a year, this can translate into hundreds, even thousands, of dollars that can be reinvested, saved, or used to treat yourself. But how do you achieve this consistently, without juggling a dozen different cards or constantly tracking rotating categories? The answer lies in understanding the current credit card market, anticipating future trends, and implementing a strategic approach to your card portfolio.

The Foundation: Understanding 2% Back Rewards Cards

Before diving into advanced strategies, it’s crucial to understand the fundamental cards that offer a baseline of 2% back rewards on all purchases. These cards are the bedrock of any successful 2% back strategy. While the market is dynamic, certain cards have historically maintained their competitive edge in this space. They typically come with no annual fee or a very low one, making them accessible and attractive for broad usage.

Key Characteristics of Top 2% Back Cards:

- Flat-Rate Rewards: The primary feature is a consistent 2% cash back (or 2 points per dollar, where points are redeemable for 1 cent each) on every purchase, regardless of category.

- No Annual Fee (or Waivable): To maximize your net rewards, avoiding annual fees is paramount. Some premium cards might offer 2% or more but come with a fee that needs to be offset by higher spending.

- Simple Redemption: Easy redemption options, typically as statement credits, direct deposits, or checks, are preferred.

- Minimum Spending Requirements: Be aware of any minimum spending requirements to earn the full rewards, though flat-rate 2% cards rarely have these.

Leading Contenders for 2% Back in 2026:

While specific card offerings can change, here are types of cards that are likely to form the core of a 2% back rewards strategy in 2026:

- Citi Double Cash Card: Often considered the gold standard for flat-rate cash back, offering 1% when you buy and 1% when you pay, totaling 2% cash back on all purchases. It has no annual fee, making it a perennial favorite.

- Fidelity Rewards Visa Signature Card: This card offers 2% cash back on all purchases, provided you deposit your rewards into an eligible Fidelity account. This is an excellent option for those already investing with Fidelity or looking to start.

- PayPal Cashback Mastercard: Offers 2% cash back on all purchases, with rewards easily redeemable to your PayPal balance. Great for frequent PayPal users.

- Wells Fargo Active Cash Card: A strong contender with 2% cash rewards on purchases and no annual fee. It often comes with a solid sign-up bonus as well.

- Alliant Cashback Visa Signature Card: This card offers a competitive 2.5% cash back on the first $10,000 in eligible purchases per billing cycle, making it ideal for high spenders. However, it requires being an Alliant Credit Union member and meeting certain checking account criteria.

Your first step is to identify which of these (or similar upcoming cards) best fits your financial habits and existing banking relationships. A single, reliable 2% cash back card can replace the need for multiple category-specific cards for general spending, simplifying your wallet and your rewards tracking.

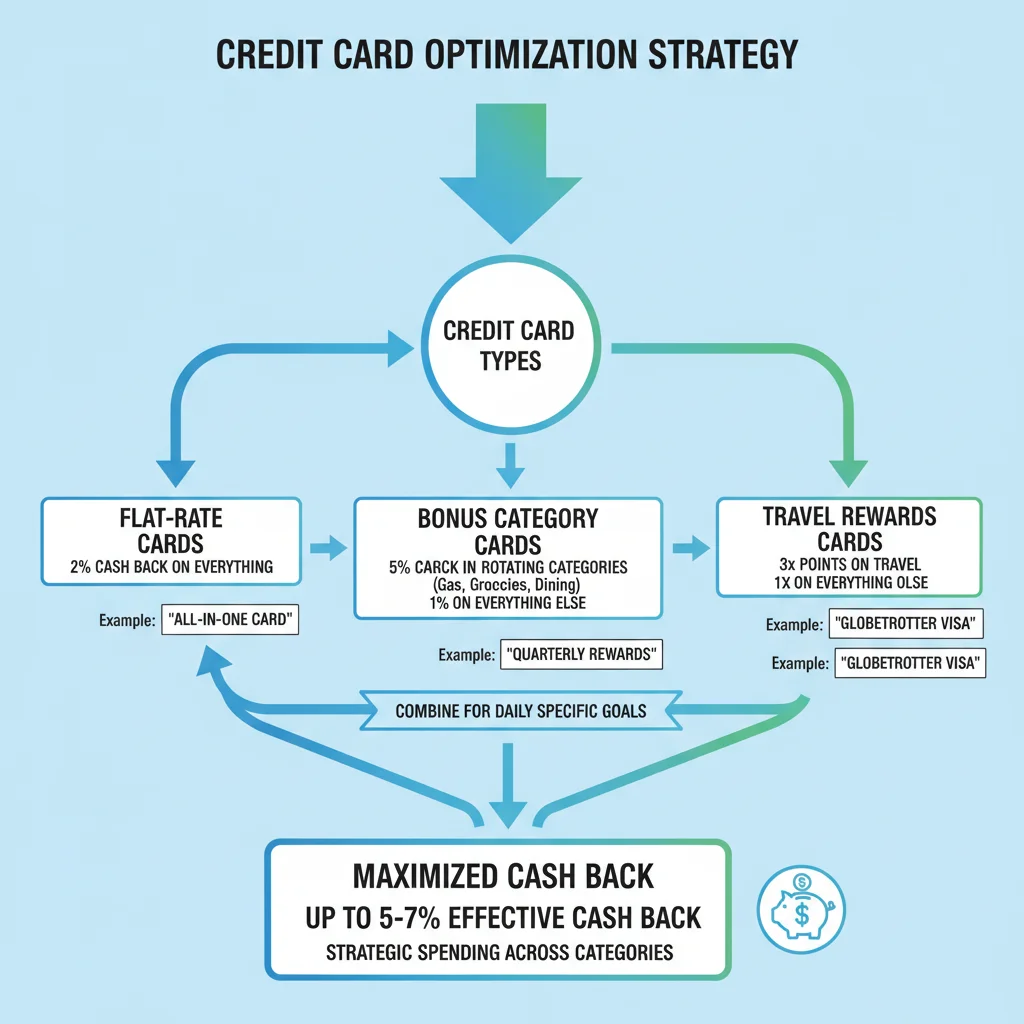

Beyond the Baseline: Stacking Rewards for More Than 2%

While a dedicated 2% cash back card is a fantastic starting point, the true mastery of credit card rewards lies in strategically combining different cards to achieve even higher returns on specific spending categories, effectively pushing your overall rewards well beyond the 2% back rewards threshold.

The Power of a Diversified Card Portfolio:

A diversified portfolio means having a few cards, each excelling in different spending categories. The goal is to use the right card for the right purchase, while still falling back on your 2% card for everything else.

- Category-Specific Cards: Many cards offer 3%, 4%, or even 5% cash back in specific categories like groceries, gas, dining, or online shopping. Examples include the Amazon Prime Rewards Visa Signature Card (5% at Amazon/Whole Foods), Chase Freedom Flex (5% rotating categories), or American Express Blue Cash Preferred (6% on groceries, 3% on streaming/gas).

- Travel Rewards Cards: If you travel frequently, cards like the Chase Sapphire Preferred or American Express Gold Card offer elevated points on travel and dining, which can often be redeemed for more than 1 cent per point, effectively yielding higher than 2% back.

- Business Credit Cards: For business owners, business credit cards often provide enhanced rewards on common business expenses, which can supplement personal spending strategies.

Building Your Optimized Card Stack:

- Identify Your Top Spending Categories: Analyze your past spending habits. Where do you spend the most money each month? Groceries, dining, gas, online shopping, travel?

- Select Complementary Cards: Choose 1-2 category-specific cards that offer high rewards in your top spending areas. For example, if groceries are a major expense, a card offering 4-6% back on groceries is essential.

- Designate Your Default 2% Card: For all other spending that doesn’t fall into a high-reward category, use your chosen 2% cash back card. This ensures you never earn less than 2% on any purchase.

- Consider Sign-Up Bonuses: Don’t overlook the value of sign-up bonuses. These can provide hundreds of dollars in cash back or points for meeting initial spending requirements, significantly boosting your overall rewards for the year.

Example Strategy:

- Groceries: American Express Blue Cash Preferred (6% back)

- Dining/Travel: Chase Sapphire Preferred (3x points on dining, 2x on travel, potentially 3-5% value)

- Rotating Categories: Chase Freedom Flex (5% on activated categories)

- Everything Else: Citi Double Cash (2% back)

By strategically applying this method, you can easily achieve an average return of 3-4% or even higher on your total spending, far surpassing the baseline 2% back rewards.

Maximizing Value: Redemption Strategies and Advanced Tips

Earning rewards is only half the battle; redeeming them wisely is equally important. The value you get from your rewards can vary significantly based on how you choose to cash them in.

Smart Redemption Options:

- Cash Back: For most 2% cash back cards, direct deposit or statement credit is the most straightforward and often the best option, as it provides a clear 1 cent per point value.

- Travel Portals/Transfers: If you’re accumulating points with travel cards (e.g., Chase Ultimate Rewards, Amex Membership Rewards), transferring points to airline or hotel partners can often yield significantly higher value (2 cents per point or more) compared to booking through the card’s travel portal or redeeming for cash.

- Gift Cards: While convenient, gift card redemptions often offer a lower value than cash back or travel transfers. Only consider this if there’s a bonus on a gift card you genuinely need.

Advanced Tips for Boosting Your 2% Back Rewards:

- Pay Your Balance in Full: This is non-negotiable. Any interest paid on your credit card balance will quickly negate any rewards earned. The goal is to profit from your spending, not pay for it.

- Utilize Shopping Portals: Many credit card companies and third-party sites (like Rakuten or TopCashback) offer additional cash back or points when you click through their portals before making online purchases. This is a fantastic way to stack rewards on top of your card’s base earnings. For example, you might earn an extra 3% cash back through a portal, plus your 2% from the card, totaling 5% back on that specific purchase.

- Leverage Manufacturer/Store Promotions: Combine your rewards strategy with store sales, coupons, and loyalty programs. A 20% discount plus 2% cash back is better than just 2% cash back.

- Referral Bonuses: If you’re happy with your cards, consider referring friends or family. Many card issuers offer referral bonuses (e.g., $100 or 10,000 points) for successful referrals, which can significantly boost your overall rewards.

- Monitor Card Benefits: Beyond rewards, many cards offer valuable benefits like purchase protection, extended warranties, travel insurance, and no foreign transaction fees. Understand and utilize these benefits to save money and enhance your financial security.

- Annual Review: At least once a year, review your credit card portfolio. Are your spending habits still aligned with your current cards? Are there newer, more rewarding cards available? Are you paying annual fees on cards you no longer maximize? Adjust as needed.

Anticipating the 2026 Credit Card Landscape

The credit card industry is constantly evolving. What works today might be slightly different tomorrow. As we approach 2026, here are some trends to consider:

- Increased Competition: Expect continued innovation and competition among card issuers, potentially leading to new and more generous rewards programs. Stay informed about new product launches.

- Focus on Digital Wallets and Mobile Payments: Rewards for using digital wallets (Apple Pay, Google Pay, Samsung Pay) might become more prevalent or offer bonus categories.

- Personalized Offers: Card issuers are increasingly using data to provide personalized spending offers. Regularly check your card accounts for targeted promotions that can further boost your rewards.

- Environmental and Socially Conscious Rewards: Some cards might start offering bonus rewards for spending with sustainable businesses or making charitable donations, aligning with growing consumer values.

- Subscription Service Integration: With the rise of subscription models, expect more cards to offer elevated rewards or statement credits for popular streaming, fitness, or delivery services.

Staying agile and informed will be key to maintaining an optimal 2% back rewards strategy in 2026. Subscribe to financial news, follow reputable credit card blogs, and regularly check your card issuer’s announcements.

Common Pitfalls to Avoid

While the goal is to earn 2% back rewards, certain missteps can quickly undermine your efforts. Be mindful of these common pitfalls:

- Carrying a Balance: As mentioned, interest charges can quickly erode even the most generous cash back. Always pay your statement balance in full and on time.

- Overspending: Don’t spend money you wouldn’t otherwise spend just to earn rewards. The purpose of rewards is to get a return on your *necessary* spending, not to encourage unnecessary purchases.

- Applying for Too Many Cards: While a diversified portfolio is good, applying for too many cards in a short period can negatively impact your credit score. Be strategic and selective.

- Ignoring Annual Fees: Always calculate if the rewards and benefits of a card with an annual fee outweigh the cost. If you’re not getting at least 2-3 times the annual fee back in value, it might not be worth it.

- Missing Payment Deadlines: Late payments can result in fees, interest charges, and a hit to your credit score, making rewards irrelevant. Set up auto-pay or calendar reminders.

- Not Understanding Redemption Rules: Some rewards expire, or have specific redemption requirements. Read the fine print to ensure you can claim your rewards when you want them.

Building and Maintaining Excellent Credit

A strong credit score is the foundation for accessing the best credit cards and their associated rewards. Without good credit, your options for cards offering 2% back rewards or higher will be limited. Here’s how to maintain an excellent credit profile:

- Payment History: This is the most crucial factor. Pay all your bills on time, every time.

- Credit Utilization: Keep your credit utilization ratio (the amount of credit you’re using divided by your total available credit) low, ideally below 30%, but even better below 10%.

- Length of Credit History: The longer your credit accounts have been open and in good standing, the better. Avoid closing old, unused accounts unless they have annual fees you can’t justify.

- Credit Mix: Having a mix of different types of credit (e.g., credit cards, installment loans) can be beneficial, but only if managed responsibly.

- New Credit: Be judicious about applying for new credit. Each application results in a hard inquiry, which can temporarily lower your score.

Regularly monitoring your credit report for errors is also a wise practice. Free services allow you to check your report from all three major credit bureaus annually.

The Long-Term Impact of Earning 2% Back Rewards

While earning a few hundred dollars here and there might seem modest, the cumulative effect of consistently earning 2% back rewards over years can be substantial. Consider the following:

- Increased Savings: The cash back can be directly deposited into a savings account, accelerating your financial goals.

- Debt Reduction: Use the rewards to make extra payments on existing debts, reducing interest paid over time.

- Investment Opportunities: For those with Fidelity or similar investment accounts, directing rewards into these accounts can compound your wealth over the long term.

- Funding Discretionary Spending: Use the rewards to pay for vacations, dining out, or other non-essential purchases, effectively making these experiences ‘free’ or heavily discounted.

By treating your credit card rewards as a legitimate income stream, you shift your perspective from simply spending to strategic financial management. This mindset is crucial for harnessing the full power of 2% back rewards and beyond.

Conclusion: Your 2026 Blueprint for Financial Rewards

Achieving a consistent 2% back rewards rate on all your credit card spending by 2026 is an entirely attainable goal with the right strategy. It involves a combination of selecting the right flat-rate cash back cards, strategically stacking category-specific cards, and mastering smart redemption practices. Remember to prioritize paying your balance in full, utilizing shopping portals, and regularly reviewing your card portfolio to adapt to changing market conditions and personal spending habits.

The financial landscape is dynamic, but the principles of smart money management remain constant. By diligently implementing this blueprint, you’ll not only maximize your credit card rewards but also cultivate a more disciplined and rewarding approach to your personal finances. Start building your optimized credit card portfolio today and watch your 2% back rewards grow into significant financial gains for 2026 and the years to come.